INDUSTRY ALERT:

Proposed Department of Education regulations could put up to 92% of proprietary beauty schools at risk of closing within the next two years. This would have a catastrophic impact across the entire professional beauty industry.

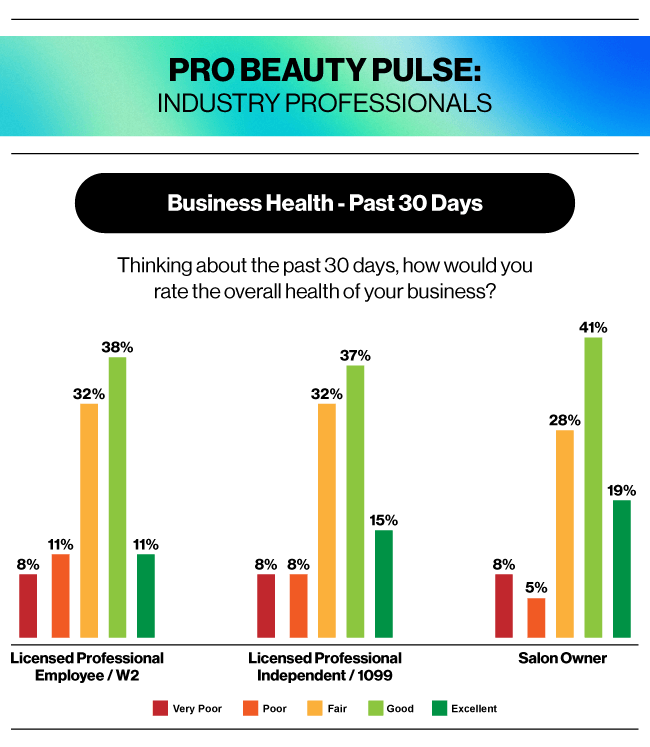

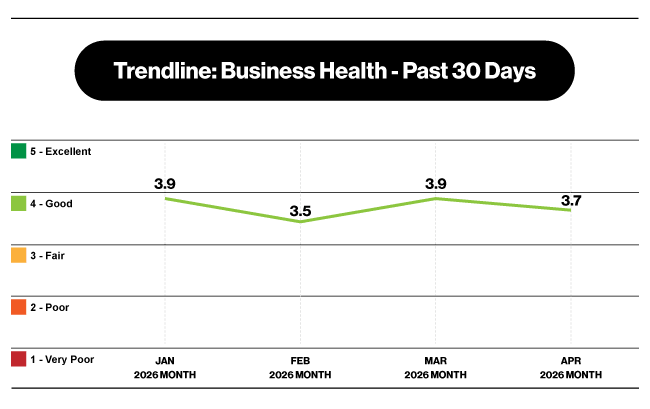

While there were minimal changes in professional community confidence this month, there was a significant decline in school community confidence. We strongly urge all salon professionals to comment in support of our industry.

Please act as soon as possible—comments shared after May 20 will not be considered.

To better understand how confident beauty professionals and beauty schools feel about their businesses, the Professional Beauty Association (PBA), in partnership with PBA Business Member Pivot Point International, created the Pro Beauty Pulse.

This monthly index tracks industry sentiment across W-2 beauty professionals, 1099/independent professionals, salon owners, and beauty school leaders. We also include data from The KIM Report, providing real-world salon performance results to complement sentiment insights.

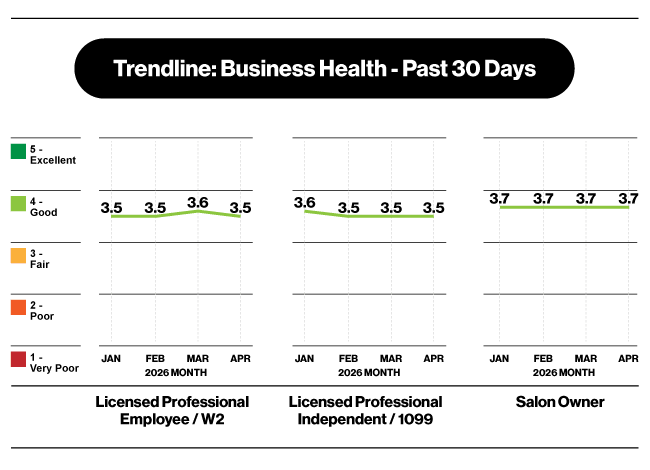

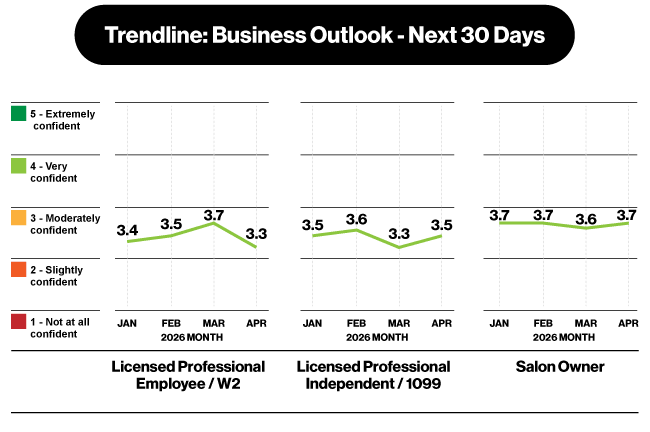

The chart above reflects industry sentiment collected in April, based on how professionals perceived their business conditions in March.

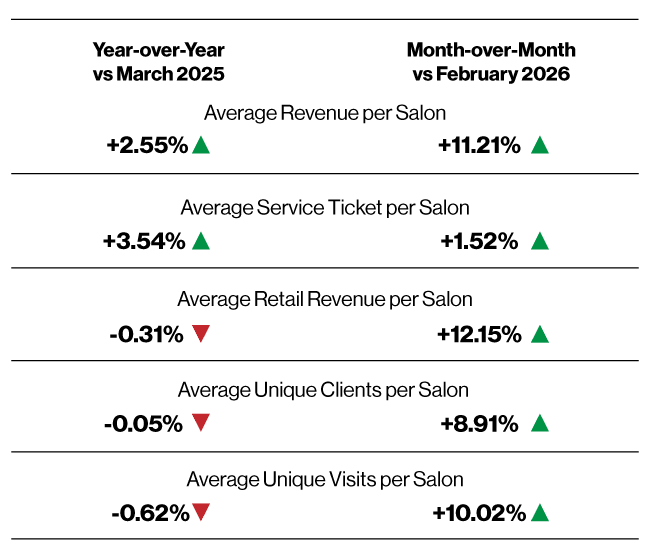

For additional context, the data below—sourced from The KIM Report—shows actual industry performance for March.

Together, these offer a clear, side-by-side comparison of salon industry perceptions versus real-world results.

Year-over-Year Performance (March 2026 vs. March 2025)

- Solopreneurs: -1.87%

- Commission Salons: +3.65%

Month-over-Month Performance (March 2026 vs. February 2025)

- Solopreneurs: -9.8%

- Commission Salons: -12%

KEY TAKEAWAY:

Growth in March was still driven more by pricing and mix than by a meaningful traffic rebound. Clients were essentially flat year over year, visits were slightly down, and services were only marginally positive. That means revenue growth came primarily from stronger tickets, with some support from color.

Note that February was a 28-day month vs March at 31, therefore a + 10% in MoM (Month on Month) comparables could be expected in volume numbers.

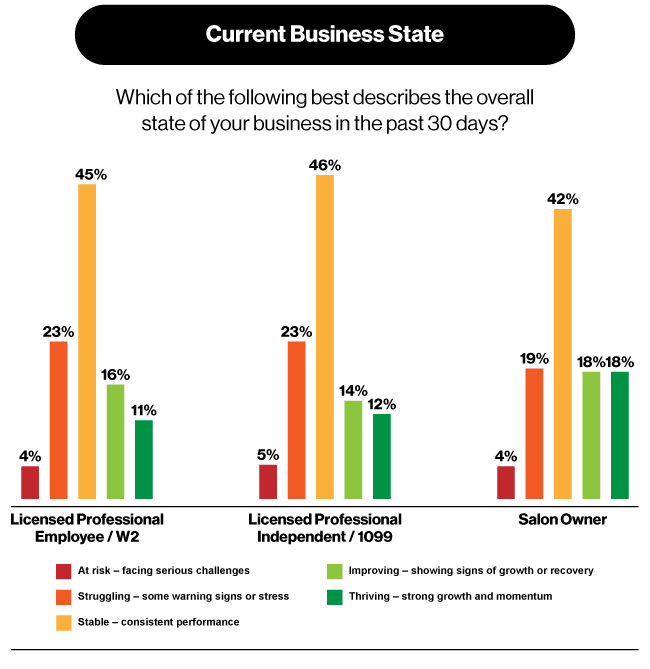

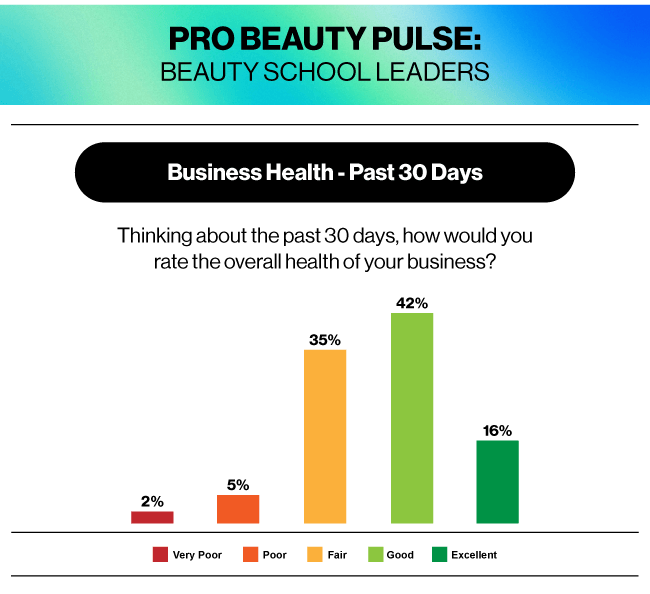

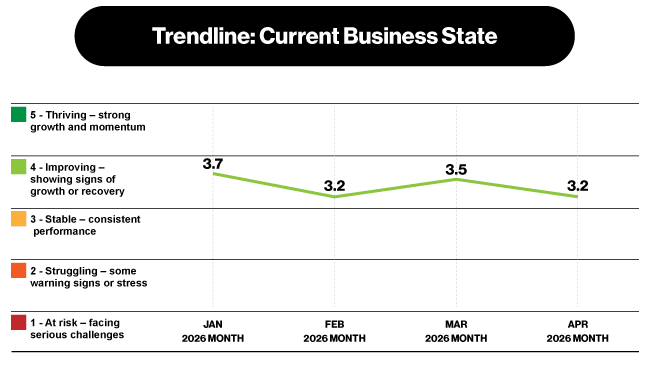

Perhaps reflecting an increased awareness of pending Department of Education regulations, April saw a noticeable shift in overall sentiment, with only 58% rating their business health as good or excellent—down from 71% in March.

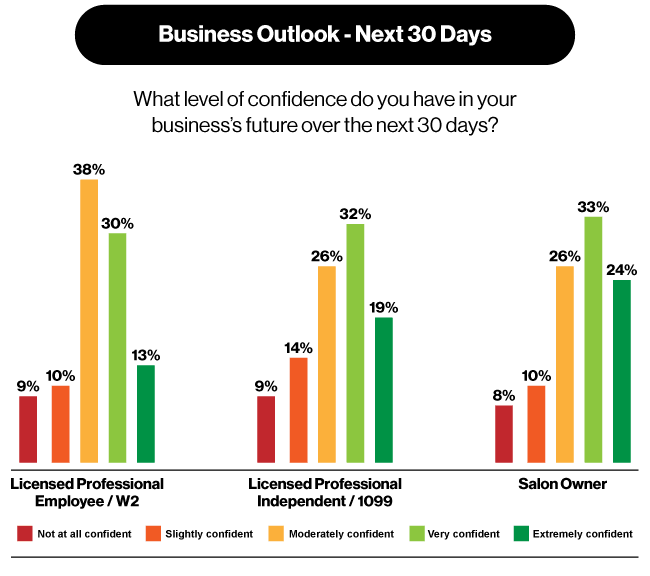

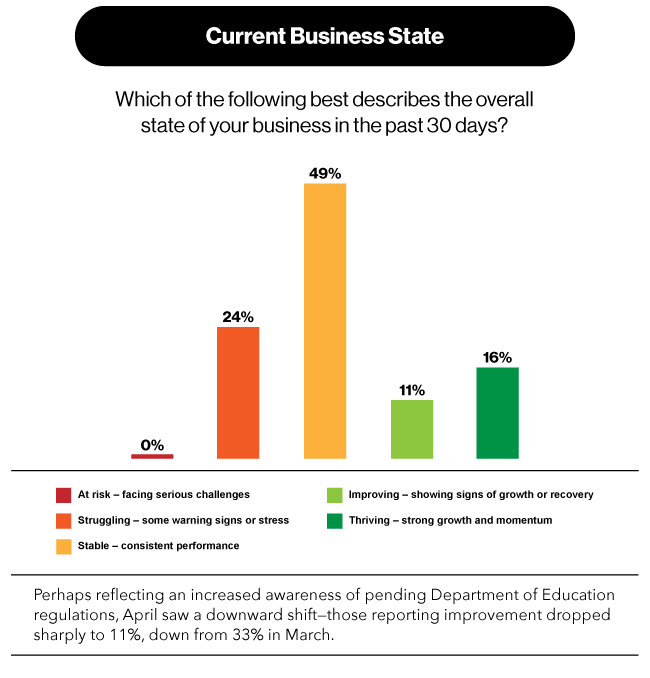

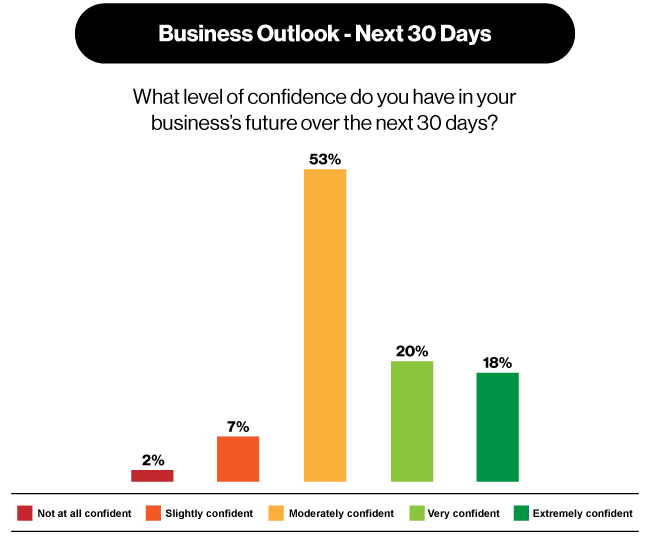

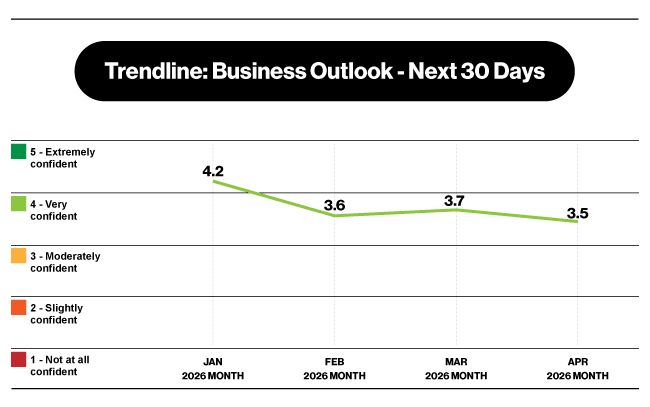

Possibly reflecting increased awareness of pending Department of Education regulations, April saw a decline in future sentiment—those reporting they were very or extremely confident dropped from 63% in March to 38% in April.

The KIM Report aggregates data from more than 10,000 salons and solopreneurs, each with 24 consecutive months on the same software platform to ensure data consistency and reliability.

KEY TAKEAWAY

Growth in March was still driven more by pricing and mix than by a meaningful traffic rebound. Clients were essentially flat year over year, visits were slightly down, and services were only marginally positive. That means revenue growth came primarily from stronger tickets, with some support from color.

Note that February was a 28-day month vs March at 31, therefore a + 10% in MoM (Month on Month) comparables could be expected in volume numbers (retail / services / clients).

STAY INFORMED

Explore more insights in The KIM Report, your source for real-world data and monthly performance trends shaping the professional beauty market.